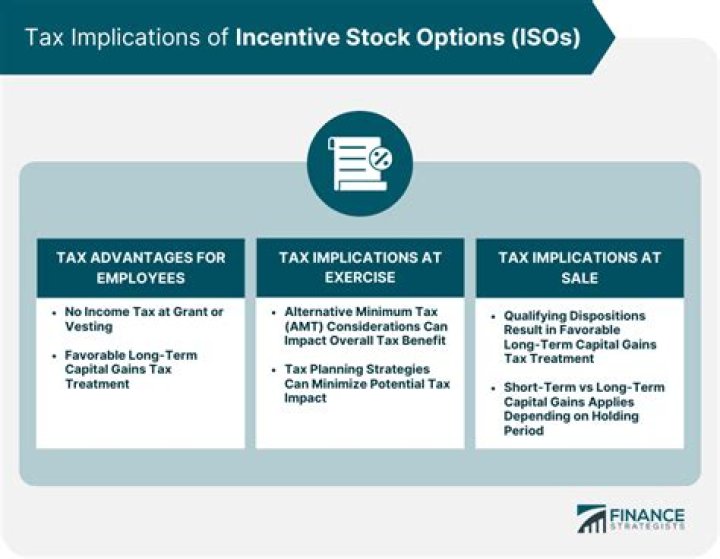

In the year that you exercise an Incentive Stock Option, the difference between the market value of the stock on the exercise date and the exercise price counts as income under the AMT rules, which can trigger an AMT liability. However, you will also generally earn an AMT credit in that year.

Does prior year AMT credit trigger AMT?

More Info On AMT Credit Carryforward Option. The Prior-Year Minimum Tax Credit lets you get back money you paid as an AMT in a prior year. You can only claim this credit in a year when you don’t have to pay AMT. You can’t use the credit to reduce your AMT liability in the future.

Does AMT tax credit expire?

This AMT credit carryforward has no expiration date. Any AMT credit carryforwards that do not reduce regular taxes generally are eligible for a 50% refund in 2018 through 2020 and a 100% refund in 2021.

When do you pay AMT on incentive stock options?

If you exercised incentive stock options (ISO) in the last several years, you may have been hit with a hefty alternative minimum tax (AMT) bill. The AMT is charged when you exercise your ISO, hold on to your shares and sell them after the calendar year in which they were awarded to you.

What’s the tax rate on an incentive stock option?

These “add-backs” are called “preference items” and the spread on an incentive stock option (but not an NSO) is one of these items. For taxable income up to $175,000 or less (in 2013), the AMT tax rate is 26%; for amounts over this, the rate is 28%. If the AMT is higher, the taxpayer pays that tax instead.

Is the fair market value of stock included in Amt?

The bargain element, or the difference between what you paid for the stock (your grant price) and what it was worth that day (the fair market value) is excluded from your ordinary income tax as one of its tax advantages, but it is included in your AMT income when you exercise your ISOs and hold onto them that calendar year.

Is the Amt taxing the spread realized on exercise?

The AMT can end up taxing the ISO holder on the spread realized on exercise despite the usually favourable treatment for these awards. First, it’s necessary to understand that there are two kinds of stock options, nonqualified options and incentive stock options.