Section 123 states that the gift deed must be signed by the donor (person giving gift) or any other person on his behalf and attested by at least two witnesses. The movable property can be gifted either by registered document or by just delivery.

Is stamp duty applicable on gift deed?

The answer is no. Neither you nor the relative will be liable to pay taxes in a case the transfer takes place through a gift deed. However, you will have to pay stamp duty and registration charges on the transaction to provide it legal validity.

Can a son claim his share in self acquired property of his father?

No son (or daughter) has legal right over the self acquired property of his father or mother. The son could however claim a share if he can prove his contribution in the acquisition of property.

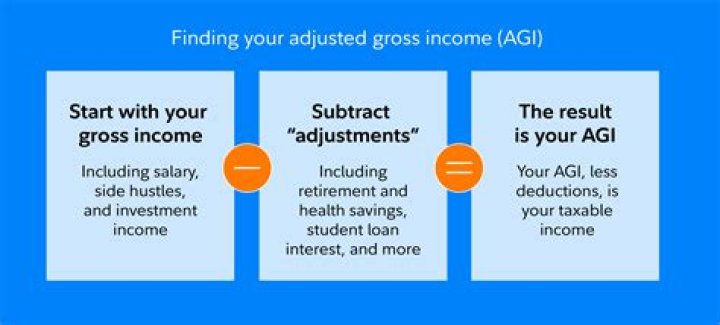

What is the tax basis of inherited and gifted property?

Tax Basis of Inherited and Gifted Property. Where an individual sells an asset that he purchased, his basis for determining gain or loss on his subsequent sale of the asset is normally his cost. Where the property was received by inheritance or as a gift, there is, of course, no cost to the recipient.

What are the rules for gifts and inheritances?

Below are some general rules governing gifts and inheritances. Gifts between spouses may be treated as a gift to the couple’s marital estate. When a spouse uses separate property to invest in marital property, the spouse’s separate property becomes part of the couple’s marital estate.

Do you have to pay tax on inherited property?

Tax savings should not be allowed to overwhelm the basic reasons for the transfer itself. This article introduces the tax consequences of selling an asset that is inherited or received as a gift. Estate planning and tax laws are complex. You should always consult with a qualified professional to assist you in such matters.

How is property inherited from a decedent determined?

The basis of property inherited from a decedent is generally one of the following: The fair market value (FMV) of the property on the date of the decedent’s death. The FMV of the property on the alternate valuation date if the executor of the estate chooses to use the alternate valuation.