It’s technically possible to get any type of mortgage loan after a bankruptcy. If you have a Chapter 13 bankruptcy, there’s no waiting period at all after a court dismisses or discharges you. FHA loans also have looser requirements compared to other types of government-backed loans.

How long after bankruptcy can I buy a house FHA?

two years

You are eligible for an FHA loan after Chapter 7 two years after discharge (the court order that releases you from liability for the debts included in the bankruptcy). During those two years, you must have re-established good credit and avoided taking on additional debt.

Can you refinance a house in Chapter 13?

With Chapter 13, FHA and VA loan borrowers may be able to refinance while they’re still in bankruptcy, after they’ve made a year of on-time payments according to their repayment plan. On conventional loans, you’ll need to wait 2 years after Chapter 13 discharge to qualify for a loan.

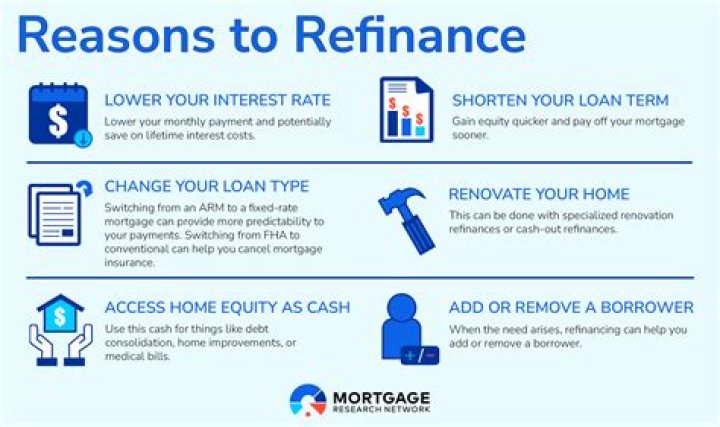

When to refinance your home loan after bankruptcy?

Refinancing after bankruptcy: Chapter 7 vs. Chapter 13. Chapter 13 bankruptcy: You are eligible one day after the discharge of your bankruptcy to qualify for a government-backed home loan. With a conventional home loan, however, you’ll need to wait two years.

Can you buy a house after filing bankruptcy?

Here are the steps on buying a house after bankruptcy, and the top things you need to know. There are two ways to file: Chapter 7 bankruptcy and Chapter 13 bankruptcy. With Chapter 7 bankruptcy, filers are typically released from their obligation to pay back unsecured debt—think credit cards, medical bills, or loans extended without collateral.

Can you get a mortgage after a chapter 13 bankruptcy?

This type of bankruptcy can stay on your credit report for up to seven years. To get a mortgage after Chapter 13 bankruptcy, you’ll need to get permission from your bankruptcy trustee, the person who oversees your repayment plan to creditors. Types of Mortgage Loans to Consider After Bankruptcy

What happens if I move out of my house after bankruptcy?

If real estate values don’t recover–or drop again–and you can’t sell the house when you are ready to move, you are still protected. You can move out and not owe them anything. (Remember though to pay your home owners association!)