If you don’t want to pay 15% or 20% in capital gains taxes, give the appreciated assets to someone who doesn’t have to pay as high a rate. The IRS allows taxpayers to gift up to $15,000 per person (a couple filing jointly can gift up to $30,000), per year without needing to file a gift tax return.

Do I have to pay capital gains tax if I don’t pay tax?

If you’re non-resident You need to tell HMRC when you sell property or land even if your gain is below the tax-free allowance or you make a loss. Non-residents do not pay tax on other capital gains.

How do I get away without paying capital gains tax?

There are a number of things you can do to minimize or even avoid capital gains taxes:

- Invest for the long term.

- Take advantage of tax-deferred retirement plans.

- Use capital losses to offset gains.

- Watch your holding periods.

- Pick your cost basis.

What kind of tax do you pay on capital gains?

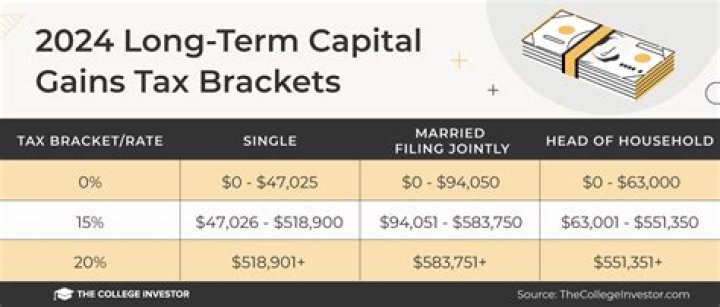

Depending on your income level, your capital gain will be taxed federally at either 0%, 15% or 20%. Let’s take a closer look at the details for calculating long-term capital gains tax. Keep in mind, the capital gain rates mentioned above are for assets held for more than one year.

Do you have to pay capital gains on your home?

Your home is considered a capital asset and is subject to capital gains tax. If your home appreciates in value, you may be liable for capital gains tax. Thanks to the Taxpayer Relief Act of 1997, you may be exempt. Here’s how you can qualify for capital gains tax exemption on your primary residence:

How to avoid capital gains tax on real estate?

One of the simplest ways to reduce your exposure to the capital gains tax is to offset the profits made from selling a home with losses that have been realized from another investment. While the Internal Revenue Service (IRS) taxes profits made from investments, they also allow investors to deduct losses from their taxable income.

How are capital gains and losses reported on a tax return?

You must account for and report this sale on your tax return. You have indicated that you received a Form 1099-B, Proceeds From Broker and Barter Exchange Transactions. You must report all 1099-B transactions on Schedule D (Form 1040), Capital Gains and Losses and you may need to use Form 8949, Sales and Other Dispositions of Capital Assets.