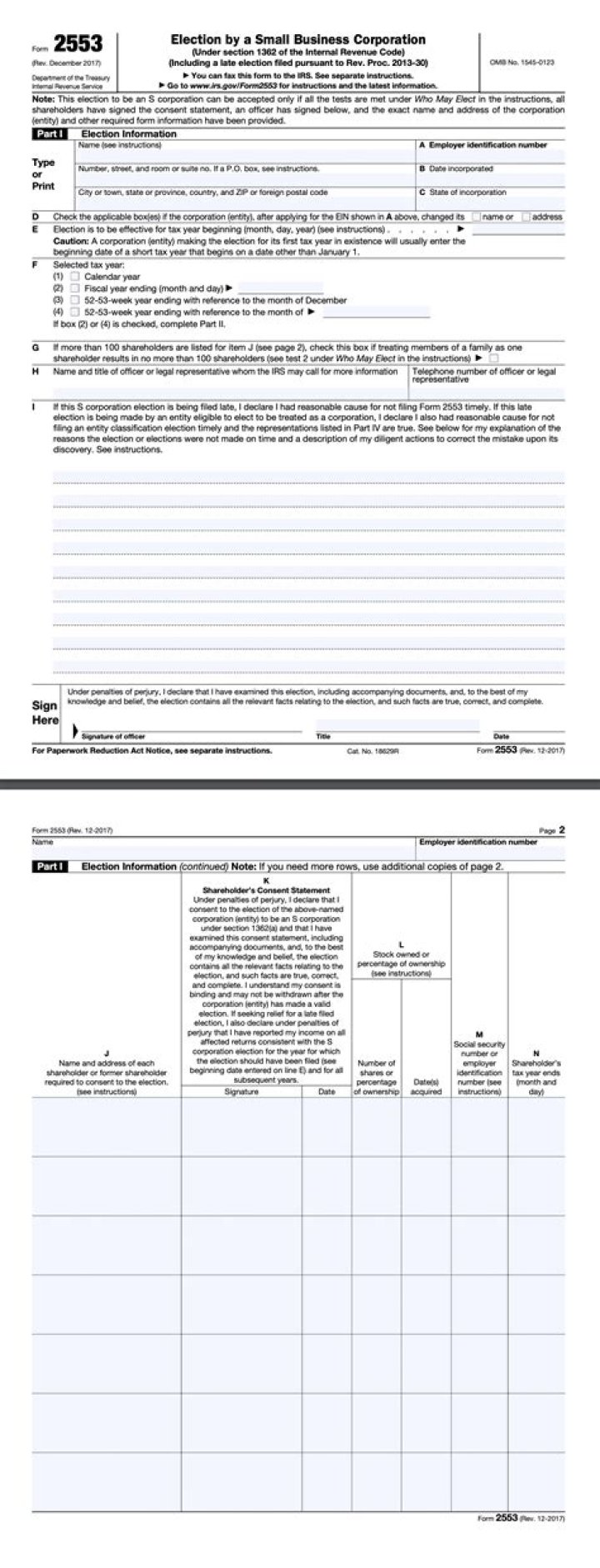

In order to become an S corporation, the corporation must submit Form 2553 Election by a Small Business Corporation signed by all the shareholders. See the Instructions for Form 2553 PDF for all required information and to determine where to file the form.

How do I request a late S-Corp election?

To do so:

- Attach Form 2553 to your current year Form 1120S, as long as the form is filed within three years and 75 days after the intended date of S-Corp election.

- Attach to a late-filed Form 1120S, which will be under the same time restrictions (three years and 75 days of intended S-Corp election date).

Can you file a late S-Corp election?

A late election to be an S corporation and a late entity classification election for the same entity may be available if the entity can show that the failure to file Form 2553 on time was due to reasonable cause. Relief must be requested within 3 years and 75 days of the effective date entered on line E of Form 2553.

When do I need to file a late 2553?

When do I need to file Form 2553 for S Corp?

You must file Form 2553 within two months and 15 days of the beginning of the tax year that you want your S corp tax treatment to start. For example, if you want your existing LLC to be taxed as an S corp in 2020, you need to file Form 2553 by March 15, 2020.

Can a single member LLC file Form 2553?

Corporations, single-member LLCs, and multi-member LLCs can all file Form 2553 so they can elect to be taxed as an S corp. However, your entity must: Be a domestic corporation or entity. Have no more than 100 shareholders (these are owners of the business).

Can a Form 2553 be attached to Form 1120?

The election can be attached to the first Form 1120-S for the year including the effective date if filed simultaneously with any other delinquent Forms 1120-S. Form 2553 can also be filed separately.