You should combine all of the 1098s directly related to the refinance and enter it as one 1098. An example of this is if you refinanced two loans into one loan. Any 1098s not directly related to the refinance should get entered separately.

Will I get a 1098 if I refinanced?

While your lender or servicer will provide you with Form 1098 (mortgage interest you paid), the existing form provides no breakout for interest that is considered acquisition debt (and is deductible) and that which isn’t considered acquisition debt (and isn’t deductible).

Will I get a 1098 if I bought a house in December?

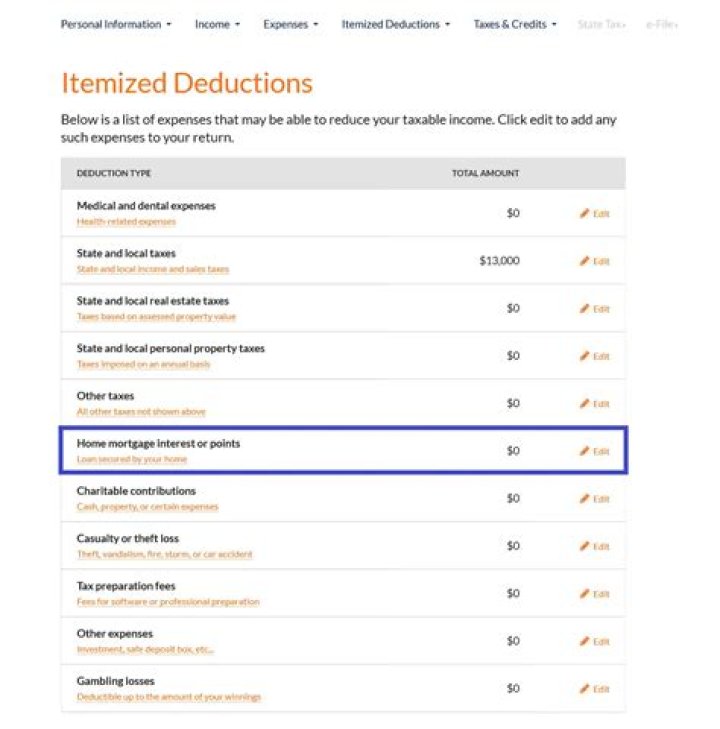

No, you will not write off your home purchase on your income tax return. However, you are able to include certain items related to your home on your tax return. If you itemize, you get to take such things as: the interest that you pay on your mortgage.

Do taxes get reassessed when you refinance?

The sale of a property can trigger a tax assessment in some places, including California. However, a refinance loan is not a sale because the property is not changing hands. So refinancing your mortgage loan won’t cause your property taxes to change.

Do you need 1098 if you refinance last year?

If you refinanced last year, you’ll have a Form 1098 from your previous lender and one from the lender you refinanced with. You’ll need both forms. Grab a calculator and add together the box 1 amount from each form. Enter the total in TurboTax as Box 1 Mortgage interest.

Do you have to have two forms of 1098?

You’ll need to enter both 1098 forms on your tax return. In TurboTax, to enter these forms 1098, please follow these steps: Follow the interview and enter your second form 1098. June 6, 2019 3:38 AM

Is there a way to override a 1098 error?

Entering an amount in the TT 1098 worksheet that’s different from the bank’s 1098 is another way to override the error–but the error is still there. Plus, it means the TT data won’t match what’s reported to the IRS.

Is there limit to amount of interest you can deduct on 1098?

If your total home debt is under $375,000 ($250,000 for married filing separate) there is nothing new for you to do in 2020. Enter each 1098 as you normally would. Under tax law, you are limited on the amount of home interest you can deduct. The limit is based on the loan amount and date of the origination of debt.