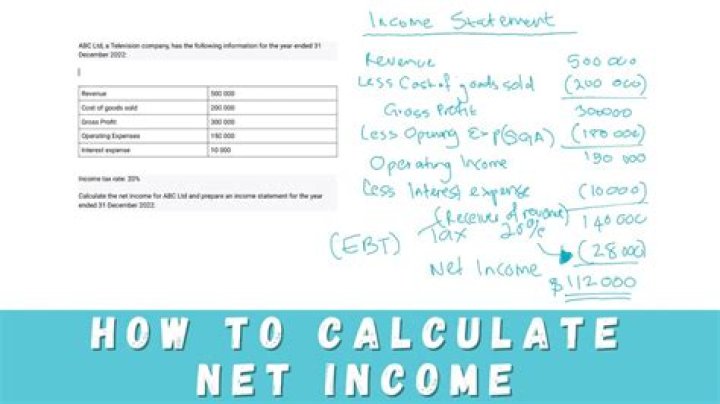

Subtract total expenses from total revenue to determine your net income or net loss. If your result is positive, you have net income. If it is negative, you have a net loss. In this example, subtract $10,000 in total expenses from $15,000 in total revenue to get $5,000 in net income.

How does a loss affect net income?

A net loss will cause a decrease in retained earnings and stockholders’ equity. A net loss will cause a decrease in the owner’s capital account and owner’s equity.

What does adjustment to net pay mean?

Adjusted net income is the excess of gross income for the tax year (including gross income from any unrelated trade or business) determined with certain modifications over the total deductions (including deductions directly connected with carrying on any unrelated trade or business) that would be allowed a taxable …

Is calculated on adjusted profit?

Adjusted earnings is a metric used in the insurance industry to evaluate financial performance. Adjusted earnings equals the sum of profits and increases in loss reserves, new business, deficiency reserves, deferred tax liabilities, and capital gains from the previous time period to the current time period.

What is Realised gain loss?

Gains or losses are said to be “realized” when a stock (or other investment) that you own is actually sold. Unrealized gains and losses are also commonly known as “paper” profits or losses. An unrealized loss occurs when a stock decreases after an investor buys it, but has yet to sell it.

Is net and adjusted income the same?

Adjusted gross income (AGI) is an individual’s taxable income after accounting for deductions and adjustments. For companies, net income is the profit after accounting for all expenses and taxes; also called net profit or after-tax income.

What is calculated on adjusted profit?

How do you calculate adjusted profit?

So if you have revenue of $200,000 and $150,000 in expenses that include $60,000 in salary and other benefits for the owner, your adjusted net profit margin is $110,000 divided by $200,000, or 55 percent.

Can you deduct unrealized losses?

In itself, an unrealized loss does not have a tax benefit and is not tax deductible. The federal tax code says that capital losses can be used to offset capital gains. If losses exceed gains, the taxpayer can take up to a $3,000 loss against other income.

What is adjustments reconcile net income?

The final category of adjustments to net income or loss are adjustments made to reflect the increase or decrease in net cash resulting from the change in the value of the financing assets or liabilities of the entity during the financial reporting period. A common financing activity is a bank loan.

How do adjusting entries affect net income?

Impact on the Income Statement Adjusting entries aim to match the recognition of revenues with the recognition of the expenses used to generate them. A company’s net income will increase when revenues are accrued or when expenses are deferred and decrease when revenues are deferred or when expenses are accrued.

How do you calculate corrected net income?

To calculate net income for a business, start with a company’s total revenue. From this figure, subtract the business’s expenses and operating costs to calculate the business’s earnings before tax. Deduct tax from this amount to find the NI.

What does net pay adjustment mean?

Adjusted net income is total taxable income before any Personal Allowances and less certain tax reliefs, for example: trading losses.

What is the difference between net income and adjusted net income?

Net income is the most comprehensive metric of profitability for a company’s operations. Net income accounts for all actual expenses and income generated for a given period, while adjusted net income reflects only those figures that would not change under new ownership.

How do you reconcile revenue?

How to Approach Revenue Reconciliation

- Record cash transactions.

- Reconcile sales data to recorded cash transactions.

- Record revenue entries using the reconciled sales data.

- Reconcile ending revenue balance sheet accounts (accounts receivable, funds in transit/clearing accounts, and deferred revenue)