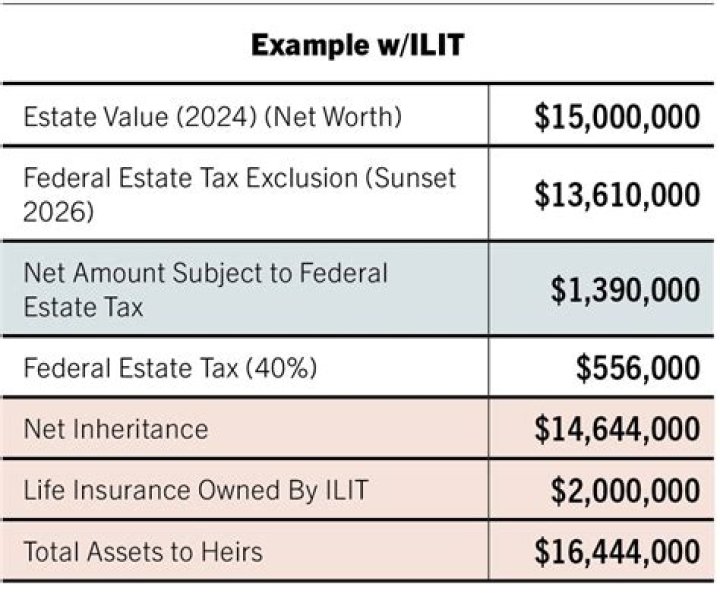

Changes to an ILIT can only be made by the beneficiaries, so the benefactor loses control of the assets before death. Furthermore, while ILIT assets are not taxed as part of the estate, they are taxed as part of the beneficiaries’ estates, consequently leaving a bigger tax burden to their descendants.

What is the purpose of an Ilit?

An irrevocable life insurance trust (ILIT) is created to own and control a term or permanent life insurance policy or policies while the insured is alive, as well as to manage and distribute the proceeds that are paid out upon the insured’s death.

Who should be the trustee of an Ilit?

2. Who can serve as an ILIT trustee? The trustee of an ILIT can generally be anyone other than the insured, although naming an “independent trustee” may offer greater flexibility for estate planning.

Do I need an Ilit?

An ILIT is a good idea if you have a significant amount of wealth and assets you need to protect after you pass. To avoid hefty estate tax and creditors, as well as set up your family after you pass, an ILIT might work for you.

How does an Ilit help you avoid estate taxes?

An ILIT can help you avoid estate taxes. Many people aren’t aware that for tax purposes, their estates might include the proceeds from their life insurance policies when they die. Depending on the value of the policy, this could invite an estate tax bill.

When is it a good idea to use Ilit Trust?

1 An irrevocable life insurance trust (ILIT) is a structure that cannot in any way be rescinded, amended, or modified,… 2 Life insurance policies are the chief assets held in ILITs. 3 There are several advantages to (ILIT), including state tax considerations, the protection of fiscally-careless… More …

What is an irrevocable life insurance trust ( Ilit )?

An irrevocable life insurance trust (ILIT) is a structure that cannot in any way be rescinded, amended, or modified, after its initial creation. Life insurance policies are the chief assets held …

Can a grantor change the terms of an Ilit?

ILITs are constructed with a life insurance policy as the asset owned by the trust. Once the grantor contributes property or life insurance death benefits to the trust, he or she cannot change the terms of the trust or reclaim any of the properties held within.