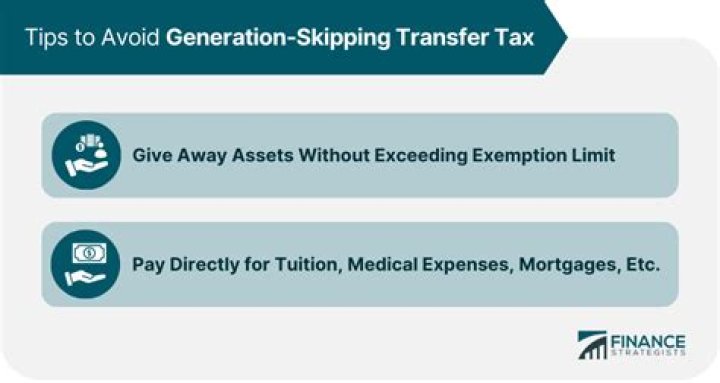

Transfers to your own children are not considered generation-skipping. The GST tax is separate from, and in addition to, the estate tax. The tax is currently calculated at a flat rate of 40 percent (equal to the estate and gift tax rate) on transfers above the lifetime GST tax exemption amount ($11.58 million).

How does the generation-skipping tax exemption work with trusts?

Generation-skipping trusts allow the settlor to avoid estate taxes that would be applied if the children, i.e., the next generation, took ownership of the assets. This means that you are allowed a lifetime generation-skipping tax exemption up to that amount against property you transfer.

How is the generation-skipping tax calculated?

The GST tax is calculated on the value of the gift or bequest, after subtraction of any allocated GST exemption, at the maximum estate tax rate for the year involved, which, for 2013 to 2017 is 40% and for 2018 to 2025, 35%. …

Do you have to pay GST on generation skipping Trust?

The 40 percent GST tax is in addition to the 40 percent gift and estate tax. As a result, generation-skipping trust distributions above the exemption threshold are subject to the 40 percent GST tax as defined by the federal tax code, as well as to any state inheritance or estate taxes that may apply.

When was the generation skipping trust tax created?

Once families started taking advantage of the GSTs’ loophole for avoiding federal estate taxes, the government updated the tax code in 1986 to create a generation-skipping transfer tax.

Do you have to pay taxes on generation skipping?

Instead, the new tax laws impose a tax at each generation regardless of whether the assets have actually been used or enjoyed by each generation. The Current Law. Thanks to recent changes in the tax law, each person may now transfer approximately $11.2 million free of this generation skipping tax.

Can a settlor be a generation skipping Trust?

A settlor, also referred to as a trustor or grantor, can establish a generation-skipping trust as part of a comprehensive estate plan that aims to minimize tax liability.