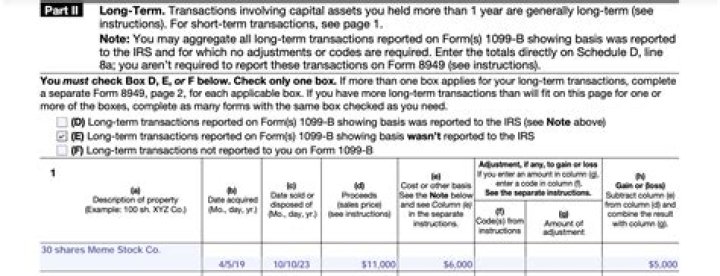

Gain or loss recognized under section 731(a) on a distribution is considered gain or loss from the sale or exchange of the partnership interest of the distributee partner, that is, capital gain or loss.

What is a Schedule k1?

Schedule K-1 is an Internal Revenue Service (IRS) tax form issued annually for an investment in a partnership. The purpose of the Schedule K-1 is to report each partner’s share of the partnership’s earnings, losses, deductions, and credits.

What does Internal Revenue Code Section 731 ( a ) mean?

Internal Revenue Code Section 731(a)(1) Extent of recognition of gain or loss on distribution (a) Partners. In the case of a distribution by a partnership to a partner- (1) gain shall not be recognized to such partner, except to the extent that any money distributed exceeds the adjusted basis of such partner’s interest in the partnership

Which is not a recognized gain or loss under Section 731?

A distribution of property (including money) by a partnership to a partner does not result in recognized gain or loss to the partnership under section 731.

When does Section 731 not apply to a distribution of property?

such distribution may not fall within the scope of section 731. Section 731 does not apply to a distribution of property, if, in fact, the distribution was made in order to effect an exchange of property between two or more of the partners or between the partnership and a partner. Such a transaction shall be treated as an exchange of property.

What is the basis to B under section 732?

As determined under section 732, the basis to B for the real property received is $3,000. (3) Character of gain or loss. Gain or loss recognized under section 731 (a) on a distribution is considered gain or loss from the sale or exchange of the partnership interest of the distributee partner, that is, capital gain or loss.