Why do you need to file Form 1041 K-1? An estate or trust is responsible for filling out Form 1041 Schedule K-1. It shows that the estate itself is passing the obligation of taxes to the beneficiary of the estate.

Who must file a California trust tax return?

Trust. The fiduciary (or one of the fiduciaries) must file Form 541 for a trust if any of the following apply: Gross income for the taxable year of more than $10,000 (regardless of the amount of net income) Net income for the taxable year of more than $100.

Why did I get a K-1 tax form?

Schedule K-1 is an Internal Revenue Service (IRS) tax form issued annually for an investment in a partnership. The purpose of the Schedule K-1 is to report each partner’s share of the partnership’s earnings, losses, deductions, and credits.

Does a trust need to file a California tax return?

Generally, a trust is subject to tax in California “if the fiduciary or beneficiary (other than a beneficiary whose interest in such trust is contingent) is a resident, regardless of the residence of the settlor.” See Cal. However, there is no time limit for the FTB to assess tax if the trust did not file a tax return.

How to file Schedule K-1 for estates and trusts?

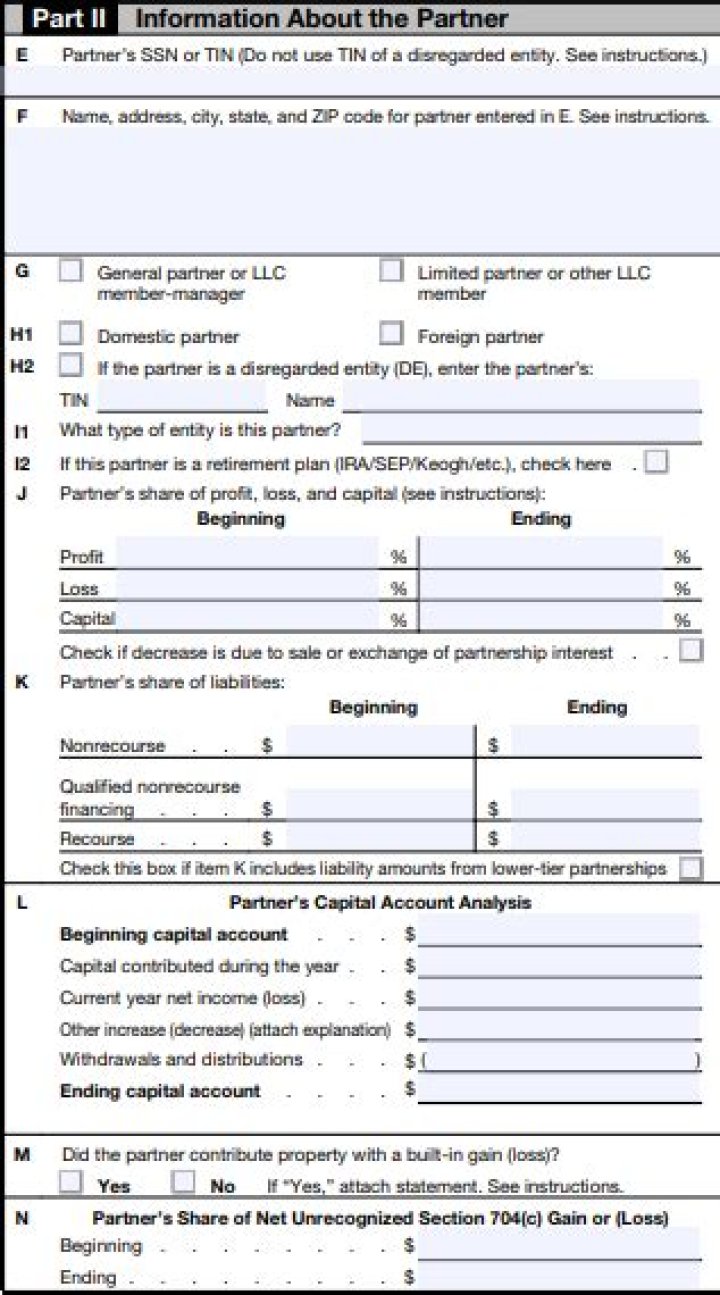

Schedule K-1, Part II is about as simple as it gets. On line F, put in the beneficiary’s TIN, and on line G, fill in the beneficiary’s name and address. In Box H, choose between a domestic or foreign beneficiary, whichever applies. If the beneficiary lives in the U.S., no further information is necessary.

How does a trust work in the state of California?

Trusts are contracts. Like all contracts trusts must declare which trust instrument. Typically, the laws of the state where the trust is established are initially chosen. Accordingly, when a California resident governs. A California court is then much interplay. It is more difficult when a

When is an irrevocable trust’s income taxable in California?

where a California resident dies and there is both a nonresident trustee and nonresident beneficiary, unless the trust contains California property (usually real estate or a business), the trust would not be subject to filing and payment of tax to California. Capital gains retained by the trust would not be

How is the residency of a trust determined?

Of the states with state income taxes, whether a trust is taxable is generally determined by one or a combination of the following criteria: Residency of trust beneficiaries (sometimes considering whether there are current distributions to the beneficiary and/or the beneficiary’s share of trust income).